- February 7, 2019 Twitter provided the Q4 2018 Earnings Report which beat analyst estimates on both Revenue and Earnings per Share.

- Forward revenue guidance for Q1 2019 was ‘light’ with an expected 20% increase in expenses for 2019

- The stock was set up as a Pattern 1 in our Earnings Strategy, reflecting a pullback if the company did not meet high expectations.

- It’s important to assess the earnings report against the Investment Thesis to validate or invalidate the reason for owning the stock.

REPORTED METRICS

- Revenue $908.8m vs estimates of $867.1m

- Earnings per Share $0.31 vs estimates of $0.25

- Monthly Active Users (MAU’s) 321m vs estimates of 323m. Q3 2018 MAU’s were 326m and 330m Q4 2017.

Q1 2019 Guidance

- Revenue $715M – $777M. Midpoint of this Range is below the midpoint of analyst expectations of $766.1M

- Expenses increase up about 20% for 2019

Twitter will not report Monthly Active Users (MAU’s) after Q1 2019. This is a key metric used by social media companies. Instead, Twitter will report a new metric ‘monetizable daily active users’. These are users which log into Twitter Apps or Twitter. com which can show advertisements.

Twitter stated, “we believe that monetizable Daily Active Users (mDAU), and it’s related growth are the best way to measure our success”.

“This change in disclosure does not impact the objectives which bring advertisers to Twitter or the information to which they have access today”…” Advertisers come to Twitter because we one of the most valuable audiences when they are most receptive, and we return a high rate of return on investment against their campaign objectives whether they are launching a new product or connecting with what’s happening on Twitter”.

Twitter reported 126M mDAU’s for Q4 2018, a 9% increase over Q4 2017.

INVESTMENT THESIS

The Investment Thesis for Twitter is founded on three areas and it’s important to compare the earnings report against the Investment Thesis.

- The power and impact of twitter as a direct communication tool.

Twitter remains a niche product without equal or threat of similar social media altering the secular trend.

2. Advertisement Engagement and monetization of the platform

Cost increases were telegraphed in Spring 2018, Twitter announced it would be facing increased Capex in various areas, improving ad formats and developing Machine Learning/AI.

On our Silicon Valley HQ Tours series we noted how the unique culture at tech companies, such as Facebook and Google, seemed inefficient with low productivity. In most other industries this culture would not function, however in technology, the culture is the cost of creativity.

Creativity is the driver of innovation which is the driver of secular trends. Secular trends evolve as society finds new ways to use platforms. If a company doesn’t innovate to sustain and evolve and drive the direction of the trend, they will be left behind. There are a number of examples of, the most significant is BlackBerry’s failure to adapt to the change in smart phones.

3. Improvements to the health of the platform translating to increased user growth.

The reduction in Monthly Active Users (326m down to 323m in the past three months) has been widely expected as a result of eliminating fake accounts to improve the ‘health’ of the platform and improve the user experience.

What does that mean at MONEYWISEHQ

You have to spend money to make money.

This seems to be the theme of big tech companies. Google and Amazon both beat analyst estimates significantly, however they also reported increased expenses for 2019 and their stock prices were similarly hit.

The ‘cost of innovation’ culture is so well ingrained in Silicon Valley that it is not going to change. IT engineers are actively headhunted and if a company changes it’s working conditions to cut costs, they will simply take a better offer elsewhere along with their experience and knowledge of a companies operations, planning and strategy.

With over 4000 employees, Twitter could be perceived as ‘bloated’ and cost increases of 20% are beyond the comprehension of analysts especially with associated forward guidance of decreasing revenue.

What needs to be seen is a monetizable conversion from the concept of improving the ‘health of the platform’ and ‘advertising engagement’ into increased revenue generation as a result of the increased Capex. The Q4 2018 earnings report is supportive of the concept, however, the forward guidance of lower revenue is contradictory.

The change to disclosure in metrics from monthly active users (MAU’s) to monetizable monthly active users (mMAU’s) will cause similar concern to analysts as when Apple changed the disclosure of iPhone sales. That concern may cause a pullback.

Earnings season market action follows one of three patterns

- Stocks run up in anticipation of strong results, then selloff when earnings don’t meet high expectations.

- Stocks remain neutral until the release then either move up or down based on the actual results

- Stocks decline as a selloff due to uncertainty of the results, then climb when results are not as bad as expected.

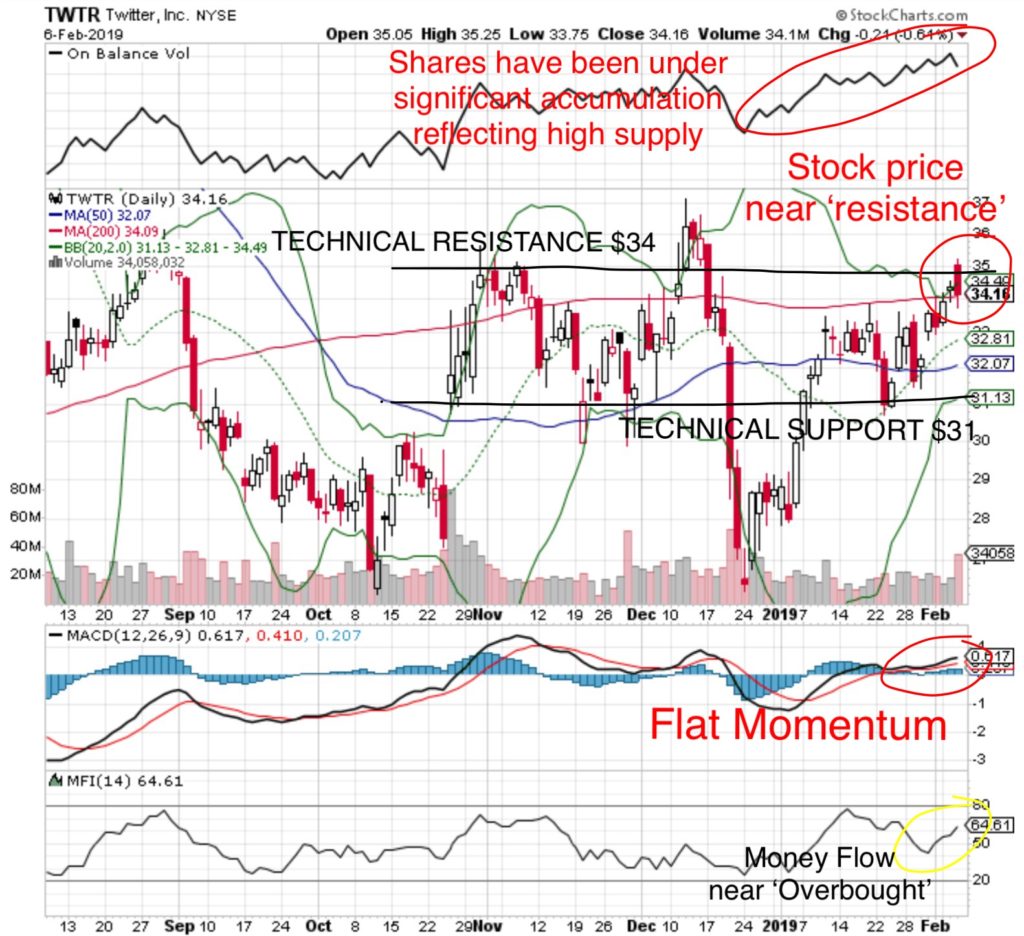

From the chart we can see

- On Balance Volume (OBV) – shares have been under accumulation reflecting a large ‘supply’ if the company didn’t meet expectations.

- Price – at Technical Resistance of $34, requiring a strong report as a catalyst to break above.

- MACD Momentum – flat

- Money Flow Index – at 65 was approaching ‘Overbought’.

- Downside risk to $31.

TWTR was set up as a Pattern 1, if the company didn’t meet high expectations, there was a high probability of a sell off.

Big Money Managers are concerned about one thing, and one thing that only, GROWTH.

If there is no growth and no catalyst then there is no reason for them to own the stock ‘right here, right now’ and it is better to reallocate funds to better opportunities. This will likely affect price momentum.

The Investment Thesis remains valid, the business is not subject to US/China trade negotiations or Interest rate increases, but it will be subject to the risk of a broader market sell off.

Strategy

First Level ‘Technical Support’ is at $31, then near $28-$29.

Accumulate shares near the low risk price of $29-$31.

Trade around a core position selling above $33.50.

Place a disciplined ‘Stop Loss’ Sell price near $28, or approximately 3%.